TPAR stands for Taxable Payments Annual Report.

What is the purpose behind TPAR

The purpose of the TPAR is to help the ATO identify contractors who are providing services who have not declared their income for tax purposes.

By filing TPAR, the ATO can cross-check the payments made to contractors as declared by the businesses in TPAR WITH the income declared by those contractors in their tax return.

Who is required to file the TPAR?

If your business provide any of the following services and hire the contractors to perform these services, then you will be required to file TPAR.

- Building and construction

- Cleaning

- Courier

- Road freight

- Information technology

- Security, investigation and surveillance

Under the TPAR requirements, payments to contractors can include subcontractors, consultants and independent contractors. They can be operating as sole traders (individuals), companies, partnerships or trusts.

If you are providing one or more of the above specified services and along with the same providing any other services, then TPAR is applicable only if the business income from the above specified services is more than 10% of the total business income.

An individual not running a business is not required to report payments made to contractors for private services.

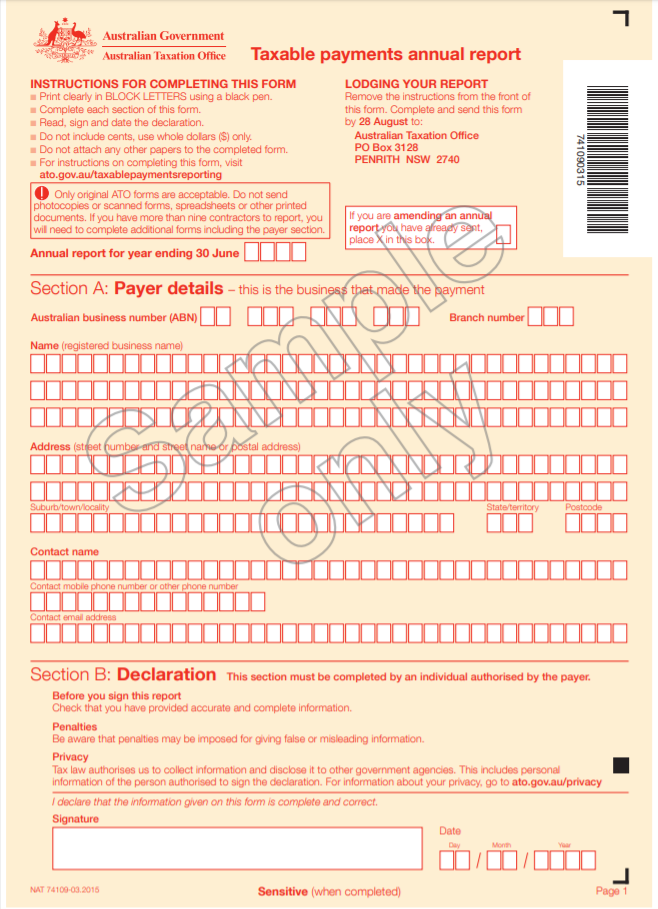

What information will be reported in TPAR?

The following information about each contractor you have paid during the year will need to be included in the TPAR report.

- Legal name of the contractor

- Address

- Australian Business Number (ABN)

- Amount you paid to them (including any GST)

Report the total payment amount if an invoice you receive from a contractor includes both labour and materials.

Payment you do not need to report

- Payments for materials only

- Unpaid invoices: Report only the payments you made on or before 30th June each year.

- Workers engaged via labour hire firm

- Payments to foreign residents for work performed overseas

- Contractors who do not quote ABN

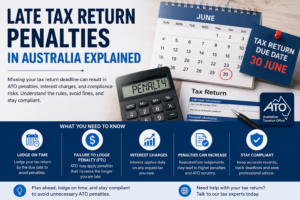

Due date for filing TPAR?

The due date for TPAR lodgement for 2022-23 financial year is Monday, 28 August 2023.

Example 1: MLQ Construction Company employ contractors to perform the construction work. The company also engage a labour hire firm. The company must report the payments made to the direct contractor on its TPAR. The company is not required to report the contractor’s payment made to labour hire firm.

MLQ also hire an independent advisor for business advisory services and compliance. As the service of the advisor is not construction, MLQ is not required to report the payment made to the advisor in the TPAR.

Example 2: XYZ Company provides commercial cleaning services and uses independent contractors and full-time employees. The company is obliged to report only the payments made to the independent contractors in its TPAR. Payment made to the employees will not come under the purview of TPAR. Hence the company is not required to report the salary payments in TPAR.

What if you fail to file TPAR?

The ATO recently issued more than 16,000 penalties for businesses who didn’t lodge their TPARs for previous years, despite receiving multiple reminders. The average penalty for not lodging was approximately $1,110.

The businesses which are subject to TPAR are required to take proactive steps to ensure that they are filing the TPAR report properly and on time.